Wealth management experiences are part of life for all of us: rich, poor or somewhere between those positions. We may not all realise that we are indeed all engaged in some level of wealth management activities. We may not all find our personal wealth management experiences pleasant. Those having planned their financial journey report wealth management experiences remembered more favourably than reported by the ‘casual journeyman’.

What wealth management experiences can we we encounter in life?

How is it that the wealth management journey is so difficult for some?

And why are similar experiences less unpleasant, less disturbing for others?

What is wealth management?

We consider wealth management to be –

‘the utilisation of the range of resources we have available,

the responsibilities we undertake, and the goals we set’

to achieve predictable outcomes as efficiently and effectively as possible.

The wealth management experience commences with accepting financial responsibility. It culminates in the attainment of the ultimate lifestyle and financial goals.

The Resources

From a wealth management viewpoint, these are generally financial in nature. They include –

- our ability to work/ derive an income,

- maintaining good health,

- access adequate capital, and

- careful cashflow management,

to ultimately attain our financial goals.

Maintaining ‘good health’ is the foundation of being able to generate adequate income to –

- fund recurrent lifestyle expenditure, as well as to

- provide investment funding for future needs.

This resource needs protection and sustenance.

Protection can be provided through healthy living. We recommend including life insurance cover for unpredictable, unavoidable events that disrupt our capacity to do our work. This strategy works equally for as employees, business owners, or investors – albeit using different personal risk products and strategies.

The provision of ‘adequate capital’ can come from a variety of sources. Some will benefit from the –

- largesse of family (gifts and/ or inheritance);

- a significant capital gain; and others

- from the reward of ‘hard work’.

All of these sources of capital will benefit from the developing and implementing investment strategies. We reiterate the benefit of supporting strategic planning efforts with relevant life insurance protection.

Your wealth may have come to you ‘on a platter’. It may be accumulating incrementally under your own stewardship. Regardless, the need for ‘cashflow management’ is usually an important exercise in the wealth management journey. Investors know that it is preferable to invest funds so as to minimise the downside risk to their portfolio. These risks can arise from market volatility – or drawdown. Market volatility is not something the investor can control. Accordingly, the better cashflow is managed, the less likely any capital drawdown will impact the future financial outcomes.

So, if these are the resources we will have available to us –

how do the responsibilities of life impact our wealth management experiences?

Our Responsibilities

Just as our responsibilities differ from each other, timing of their impact on our wealth management experiences also differs. In wealth management speak, this is referred to as sequencing risk. The responsibilities we are concerned with in this article are financial. However, the type and extent of those financial impacts may emanate from other considerations. The responsibilities that will make a demand on our wealth management process include –

- family,

- home,

- business,

- education

- and so on.

The responsibilities of ‘family’, start with the basics of life. Food, clothing and shelter are the primary responsibilities we accept. Personal responsibilities may extend well beyond the basics and include matters such as –

- lifestyle ‘luxuries’,

- health matters,

- carer duties, and possibly even,

- financial commitments (of others within our sphere of influence).

The ‘home’ part of the equation may involve a mortgage (or rent), that bring continuous financial responsibilities. These will vary in nature according to where we are in the life continuum, whether –

- single,

- partnered,

- with/ without children,

- under care/ caring, or

- in retirement.

Those with a ‘business’ is part of their responsibilities, the financial obligations will extend beyond personal needs. Here they will embrace the requirement to stay financially viable – and able to support the business if unexpected duress is experienced.

The responsibility to ‘education’ can also be multi-faceted: furthering your own education; and/ or providing for the career preparation of children or other dependants.

Some wealth management goals

There is a saying that ‘failure to plan, is planning to fail’. If we want to plan for a successful journey of wealth management experiences, we need to set a goal(s). Setting goal helps us to know where we are trying to go – and when we have arrived! They may focus primarily on what might be called ‘end goals’, but they should also include some ‘milestone measures’ that reassure us that we are on track for that end goal.

As you read through the ‘Our Responsibilities’ section above, there were no doubt, several goals that came to mind. Some of those could have been:

- age at retirement;

- family size;

- location of principal residence;

- preferred schooling arrangements;

- vehicles;

- recreational pursuits; and

- career aspirations – just to name a few.

Having set the goals and formulated the plan, the wealth manager can restart the journey with a clearer vision of where they are heading.

What will the journey be like?

Perhaps like an Ocean Cruise:

Starting out slowly, progressing along a level plane (with occasional turmoil); and arriving in a relaxed state of mind?

Perhaps like Air travel:

Starting with a steep climbing take-off; cruise at a planned level (with occasional turbulence); and then slow decline to the destination, but retaining some level of anxiety about the journey?

…or more like a Road Journey (through mountainous terrain):

Navigating through the ‘local’ streets, on to a freeway, then up and down hills and mountain ranges – and so on? … we’re sure you get the picture!

In this ‘road journey’ analogy, the wealth management experiences of this journey might be compared, –

- taking Economic Cycles as the ups, downs and twisting through mountain ranges;

- Investment Trends as the variation of road speeds in urban and rural areas or on highways in progressing towards the journey’s end; and

- Market Events are like the roadworks, RBTs and traffic congestion we might encounter along the way.

Planning, research and preparation improve the chances of a successful journey

Drivers with some years of experience are familiar with the process of planning the journey, checking that the route chosen is likely to be clear, and ensuring that the vehicle is up to the challenge. Likewise, wealth managers are encouraged to look at these elements and anticipate the long-term with clear goals and objectives – knowing the checkpoints along the way that tell you that you are progressing in the right direction. The important part of this analogy is to ensure that your financial journey is even better planned that your driving holidays might typically be (and one muses whether the ‘are we there yet’ question might be asked just as frustratingly as happens in the family car?).

What are economic cycles, investment trends and ‘market’ events?

Economic Cycles

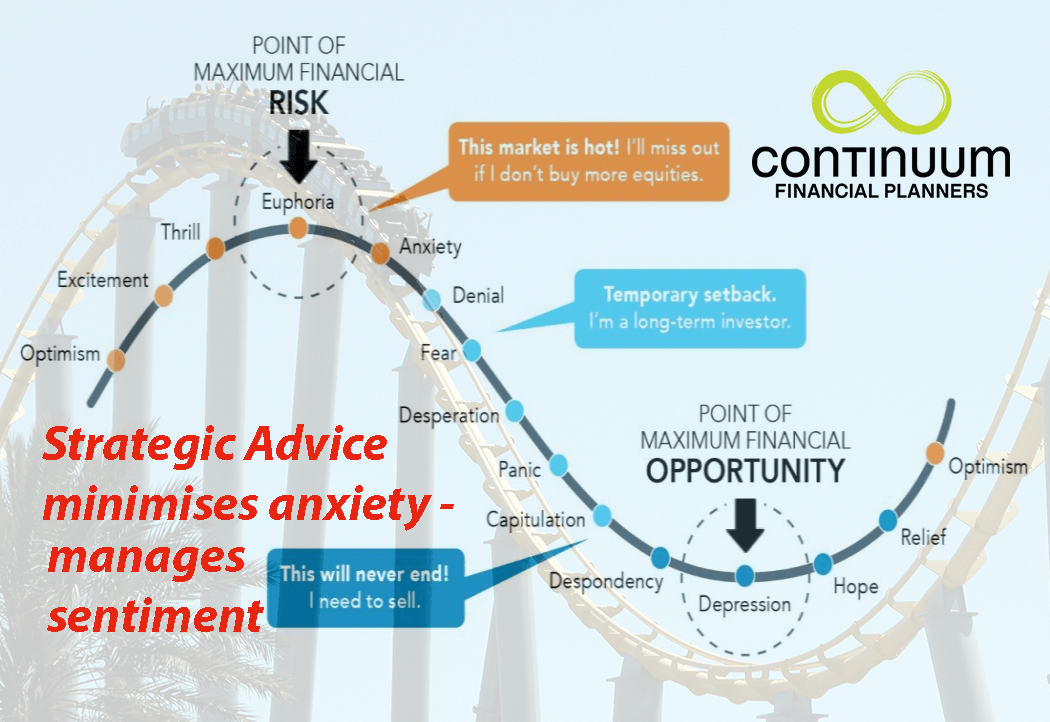

..are those recurrences of economic activity that favour investment in particular classes of assets at different times: sometimes it is property that performs better than the rest, sometimes shares, sometimes bonds and yet other times, cash. It can be difficult to determine which part of the investment cycle any particular asset class is in as there are occasional ‘noises’ that suggest they are in one phase when in fact it is merely a pause in the continuation of the recent phase.

This is at least one sound reason for diversifying a portfolio: whilst this strategy won’t provide the investor with the full benefit of the currently-performing asset class, it will allow some participation in that asset’s run – at the same time sheltering the portfolio from the full downside of the least performing asset class.

The cycle is sometimes reflected on an ‘investment clock’ – but no matter how it is portrayed, it cannot be ignored: an asset class that is the high performer for one period is unlikely to be the ‘star performer’ the following period. On the other hand, if you are holding an asset that is an under-performer, ‘cycle theory’ suggests that by holding it for an appropriate period, it will ‘take its turn in the sun’!

Investment trend

is the direction in which the aggregate value of the assets being measured is heading. An old investment expression is that ‘the trend is your friend’ – and looking at equities and property as asset classes over the past one hundred plus, years the truth of that expression is quite obvious.

[That is not always the case regarding the short-term trend of course!] The Long Term Investing Report published by the Australian Stock Exchange Limited in 2012 shows at Exhibit 2, that whilst the range of investment assets utilised in Australia has performed fairly disparately, the performance for shares and property are fairly similar over the long term. The certainty of the trend dictates the period of time for which any particular asset class should be held as a minimum term: and it is the statistic that tells us that equities and property should be bought as long-term sectors of a portfolio. In this context, a long-term investment in these asset classes should ideally be held for a period of not less than 5 years – and preferably 7 years: longer would give more reliable outcomes.

How does this come about? It is a combination of understanding the cycles mentioned above; and the periods for recovery from significant events: and analysts can tell us how long an average ‘down-cycle’ runs – and how long an ‘up-cycle’ is required to ‘get our heads above water again’! Put these issues together and the terms above become essential.

‘Market’ events

are those happenings that economist Dr Don Stammer often refers to as ‘the X-Factor’: the event/ occurrence that we usually associate with misfortune/ misadventure and that will bring unstuck the best calculation of anticipated results for a forecast period. They could also be events that give an unexpected boost to markets – though these events are less frequent historically.

We mentioned some of the more typical events in a recent article in our website Library, including –

- Natural disasters;

- Geopolitical activity;

- Terrorist activity; and

- Financial market upheaval.

Usually these events are unpredictable as to timing and ‘size’ (or effect): sometimes they affect the markets for a very brief period; in other cases, the effects are prolonged.

Looking for a tour guide for your investment journey?

Continuum Financial Planners Pty Ltd has a number of experienced advisers available to take you through the financial planning process that should improve your wealth management experiences and result in attainable financial goals and objectives, based on the resources you will be able to bring to bear.

Make an appointment with one of our experienced advisers –

- to see what you can achieve towards your own financial independence – and

- to provide for those who are dependent on your success; by

- phoning our office on 07 3421 3456, or

- at your convenience, use the linked Book A Meeting facility.

Our team work to the mantra – ‘we listen, we understand; and we have solutions’

that will be delivered in documented ‘personalised, professional wealth management advice’.

(This article was originally posted by us in April 2011. It has been occasionally been refreshed/ updated most recently, in February 2025.)