Fixed Interest: Stability, Income and Portfolio Balance

This asset class guide to fixed interest is designed to help our clients better understand its role and effectiveness in portfolio construction.

When markets are volatile, many investors ask the same question: “Should I have more in fixed interest?”

Fixed interest investments – commonly known as bonds – are a core component of diversified portfolios. They are not designed to be exciting; rather, they provide stability, income and risk management. For newer investors, those planning for retirement, and retirees alike, understanding how fixed interest works can improve confidence and decision-making.

What Is Fixed Interest?

A fixed interest investment is essentially a loan made by you, the investor, to:

- The Australian Government

- A state government

- A bank, or

- A company

In return, the issuer agrees to:

- Pay regular interest (known as a coupon)

- Return your capital at a specified maturity date

Examples include Australian Government Bonds issued via the Australian Office of Financial Management and bonds traded on the Australian Securities Exchange.

Why Fixed Interest Is Used in Portfolios

Fixed interest is not typically used to chase high returns. Its primary roles are to:

- Reduce portfolio volatility

- Preserve capital

- Provide a consistent income stream

- Diversify away from shares

Research consistently shows that portfolios including high-quality bonds tend to experience smaller declines during equity market downturns compared with share-only portfolios—an increasingly important consideration as retirement approaches.

The Benefits of Fixed Interest Investments

1. More Predictable Income

Bonds provide regular interest payments that can:

- Support retirement cash flow

- Supplement pension entitlements

- Provide stability during market volatility

Government bonds, in particular, are generally considered highly secure due to sovereign backing. For investors prioritising income certainty over growth, this predictability is valuable.

2. Lower Volatility Than Shares

Shares can experience significant price fluctuations, whereas bonds typically exhibit more stable behaviour. This makes fixed interest particularly suitable for:

- Investors approaching retirement

- Those uncomfortable with market volatility

- Portfolios seeking smoother return profiles

Lower volatility can also help reduce emotionally driven investment decisions during market downturns.

3. Diversification During Market Stress

High-quality government bonds often behave differently from shares, particularly during periods of economic stress.

For example, during the Global Financial Crisis, many government bonds increased in value while share markets declined.

While diversification does not eliminate risk, it can meaningfully reduce overall portfolio volatility.

4. Improved Yields in the Current Environment

Following an extended period of low interest rates after the GFC, bond yields have risen materially in recent years. Higher yields result in:

- Increased income

- Improved forward return expectations compared to the 2010s

This shift has renewed interest in fixed interest among investors, particularly those focused on income and capital stability.

The Risks and Limitations of Fixed Interest

It is important to recognise that bonds are not risk-free. They carry different risks to shares.

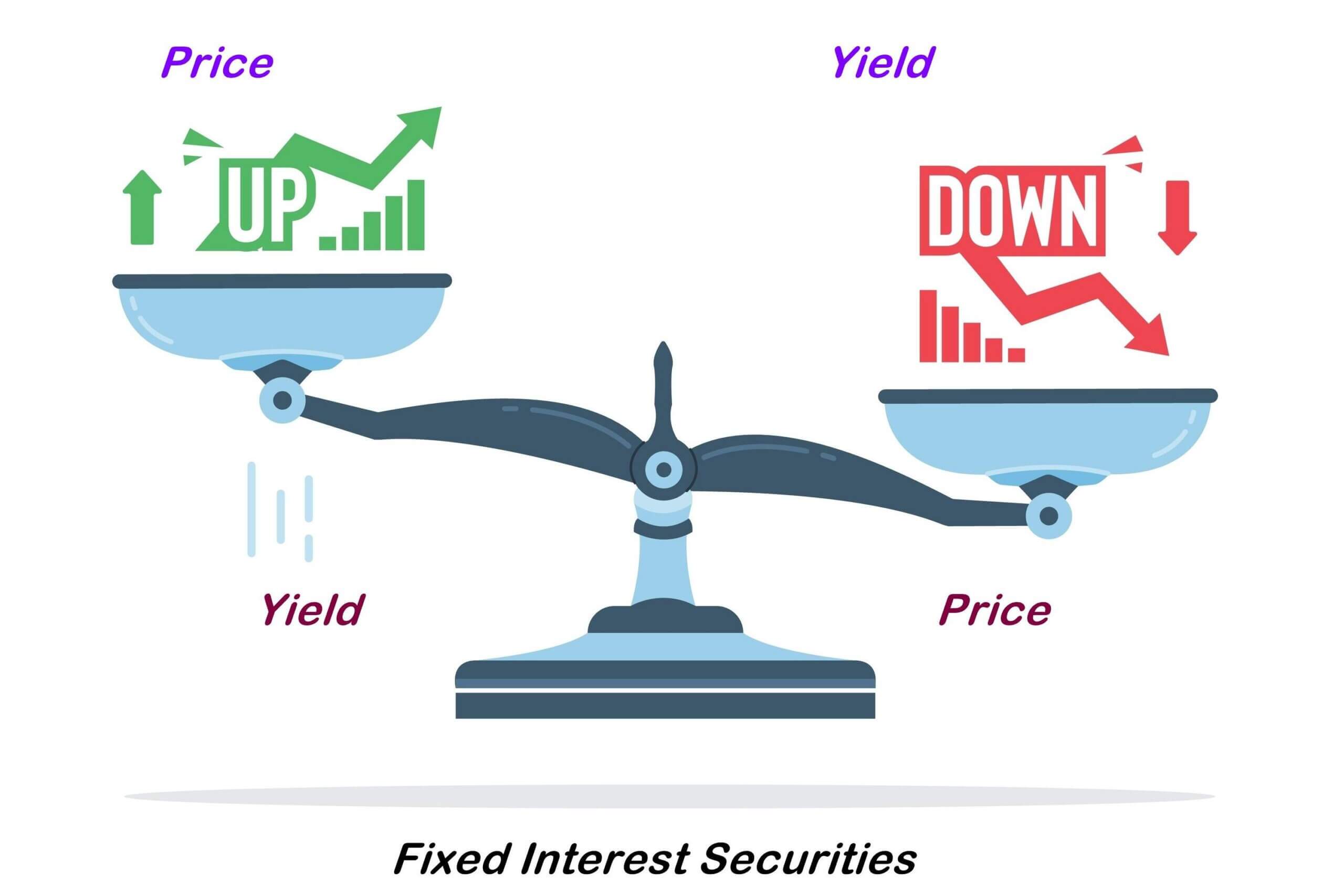

1. Interest Rate Risk

When interest rates rise, bond prices fall.

In 2022, global bonds experienced one of their weakest years in decades due to rapid increases in interest rates. Longer-term bonds are generally more sensitive to these changes.

2. Inflation Risk

Inflation reduces the real value of fixed interest payments.

Inflation-linked bonds can help mitigate this risk, although they often begin with lower yields.

3. Credit Risk

Corporate bonds depend on the financial strength of the issuer.

Higher-yielding bonds typically carry higher default risk, which is why careful selection and diversification are critical.

4. Lower Long-Term Growth Than Shares

Over the long term, shares have historically delivered higher returns than bonds.

For younger investors, holding excessive fixed interest may limit long-term wealth accumulation.

How Fixed Interest Fits at Different Life Stages

New Investors

Can benefit from –

- Helps smooth early investment experiences

- Builds confidence during market volatility

- Reduces large portfolio swings

Growth assets will generally remain the dominant allocation at this stage.

Pre-Retirement Investors

In the decade leading up to retirement, fixed interest becomes increasingly important. It can:

- Reduce sequencing risk

- Protect capital before retirement

- Improve portfolio balance

Gradually increasing exposure is a common and prudent strategy.

Retirees

For retirees drawing income from their portfolios:

- Stability becomes more important than maximum growth

- Capital preservation is critical

- Avoiding forced sales of growth assets during downturns is essential

A well-structured allocation to fixed interest can provide a buffer, allowing growth assets time to recover.

The Bottom Line

Fixed interest investments are not designed to outperform shares over the long term. Their purpose is to:

- Provide income

- Reduce volatility

- Preserve capital

- Enhance diversification

They may underperform when:

- Interest rates rise rapidly

- Inflation remains elevated

- Share markets are strongly rising

For most investors, the key question is not whether to include fixed interest—but how much, and in what form.

This depends on your:

- Time horizon

- Income requirements

- Risk tolerance

- Stage of life

A tailored approach remains essential.

Understand how fixed interest fits your portfolio

The role of fixed interest within a portfolio will vary depending on your goals, time horizon and income needs. If you would like tailored advice on how to structure your investments to balance growth, income and risk, arrange a meeting with one of our experienced financial advisers: either

- phone our office on 07-3421 3456, or

- at your convenience, use the linked Book a Meeting facility.

(This article was first posted by us in March 2026.)