A key financial priority for many of us is supporting the education of our children or grandchildren. Providing children’s education funding opens opportunities, standing them in good stead for life.

Australia has a strong education system, designed to support your goal to set your children (or grandchildren) on that path to a rewarding future. To achieve this, education options include –

- Public schooling (for any or all school years),

- private or independent schooling, and

- tertiary education.

It’s not realistic to put a dollar sign on the value of your child’s or grandchild’s future. Nevertheless, calculating the cost of their education can help you to estimate the level and type of schooling you will be able to afford them.

With private schooling, fees are a major cost and have trended faster than the rate of inflation. It’s also worth considering how the costs compare across school sectors if you are in two minds about school type.

Education costs are broader than school fees alone. You may need to factor in the costs of –

- outside tuition,

- school camps,

- transport,

- uniforms,

- electronic devices, and

- sports equipment.

The costs of these and other ancillaries mount up over the 13-year schooling journey.

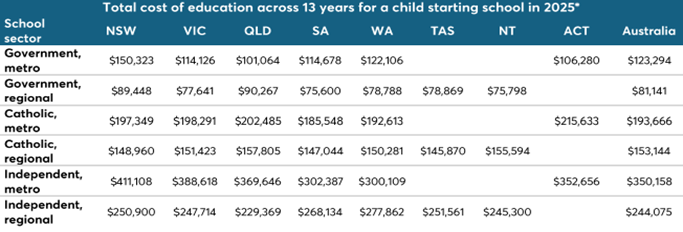

Total estimated cost of education for a child starting school in 2025*

*Estimates of future long-term education costs projected over a 13-year period are provided as a guide only and are population-weighted. The actual cost of education for a particular child or school sector or period may exceed these estimates. Source: Futurity Investment Group Planning For Education Index 2025.

It doesn’t stop there though. Post-secondary pathways could see your child or grandchild consider a slew of avenues ranging from –

- University, through to

- Vocational Training where course duration and costs vary depending on course type.

The HECS-HELP study assistance loan is an option to delay payment of the core course fees. It doesn’t fund associated costs such as textbooks and possible accommodation relocation costs. Be mindful that the HECS- HELP debt could have a long-term impact on your dependent pursuing –

- future goals (personal, business, or professional), and

- life events such as home ownership.

Each choice of education direction involves a much different financial investment. What you choose will come down to –

- affordability, and

- your own view of what is best for your children.

Regardless of your choice, a range of financial options and savings are available to support your children’s education needs.

It sounds overwhelming and probably is, given that it might not be something that you’re even considering at this stage. Planning and building a strategy to fund children’s education needs will ensure adequate cashflow and budget are provided.

Know your options

An obvious bit of advice is to do due diligence and weigh up the benefits and downsides of various strategies.

Investing in a child’s name is generally not a sensible option – as any income (over $416) will be heavily taxed. We refer to taxation risks to the strategies in the 5 Options below.

The golden rule for most financial plans is to establish and implement your plan as soon as possible. More time will help you maximise your returns and boost your savings. With that in mind, here are five options you might consider:

1. Take advantage of a home loan offset account

An offset account is a bank account linked to your home loan. Using it to save for your children’s education can be tax-effective and reduce the interest paid over the term of your loan.

Effectively, any money saved in the account earns an after-tax interest rate equal to the home loan rate, which is usually substantially higher than interest received taxed at your marginal income tax rate, as offered on term deposits or similar.

Self-discipline is the big challenge in using an offset account.

An often-over-looked option is the structure of an education bond. Designed to facilitate the entirety of an individual’s educational journey, education bonds can be contributed to by anyone and are taxed internally at the company tax rate of 30%. Careful portfolio selection can further reduce the effective rate, potentially down to around 23%.

2. Investment or education bonds

Investment bonds are investments through which you ‘lend money’ to governments or companies for potential capital growth and tax benefits. There is usually a minimum amount you must invest. The nominal tax rate on investment bond earnings is up to 30%, which is advantageous for higher-income earners. Usually, subject to certain rules, if you hold investment bonds for at least 10 years, your entire investment earnings will be ‘tax-paid’. Withdrawals after the 10 year investment anniversary will be free of personal tax.

Education bonds are a special type of investment bond that must be intended for the purpose of saving for education. In spite of this, the capital invested is not locked in for educational purposes only. If circumstances change and other needs arise, funds are accessible for any purpose at any time. In this circumstance, control over how and where the money is invested is retained by the Principal until it is withdrawn.

Education bond benefits include –

- features and tax advantages of conventional investment bonds,

- additional educational tax advantages,

- estate planning features, and

- the freedom to designate numerous beneficiaries.

The nature of the structure requires a beneficiary/ies to be nominated. In the event that the bond owner passes away, benefits can still be maintained via the bond guardian.

Australian tax law enables the education bond provider to receive a tax deduction for certain educational expenses. The bond owner will receive the value of that deduction in the form of a rebate when withdrawals are made to cover education costs.

3. Term deposits

Term deposits are one of the most well-understood and simplest ways of earning interest on savings. They offer a fixed interest rate over a specified period, typically for one or two years. They will typically be opened conjointly with a parent or grandparent, often as trustee for the child. On termination, you can choose to roll them over into a new term deposit. A new interest rate will apply, which may be lower at the relevant time.

Be aware though, that interest income earned is generally required to be declared in the name of the adult taxpayer.

4. Managed or Exchange Traded Funds (ETFs)

Investing in managed funds presents an option if you are able to invest over a reasonable term. A term of say three to ten years would be appropriate to this investment asset class.

Managed funds with exposure to the share market, property or fixed-income assets, or a diversified asset allocation are available. They generally require you to have a minimum amount of money already available to invest. An establishment fee may apply; and there will be ongoing investment management fees.

Some managed funds are listed on the Australian Stock Exchange (ASX) and are known as Exchange Traded Funds (ETFs). They can be bought and sold like other ASX shares. This means that you can easily increase your holding as you can afford it, or sell if needed.

Beware operating these accounts in the name of an adult as trustee for the child. In that circumstance, the adult may be held liable for tax payable on the income earned. Capital Gains Tax (CGT) is usually applicable when you sell – and could be a significant cost.

You should read and understand the risks and returns expected from these investments over the timeframe you’re planning to invest.

5. Invest tax-effectively

If you’re investing with an adult ‘partner’, it might be worth considering in whose name you should invest your funds. It can be more effective to invest in the name of the person paying the lowest rate of income tax. You should note to monitor and review this –

- should a job change or promotion alter your relative tax situations, or

- if your relationship changes.

Achieving peace of mind

If you’re starting early, saving for education will be a medium to long-term effort. Some of the investment options listed above may experience occasional periods of negative returns. This possibility suggests that reducing risk while optimising your savings might call for –

- some diversification of your investment portfolio –

- allocating your savings across several types of investment, and

- Invest over a five to 10-year timeframe.

Educational expenditure isn’t generally regarded as an activity that can be managed in a tax-effective manner, but it can be done and can allow you to re-allocate capital to other priorities is added bonus.

Continuum Financial Planners can help

If you are anxious about the prospect of providing the education that you want to provide for your child, we can provide helpful guidance and advice. Our experienced advisers have provided strategies to many families over the years. To benefit from our experience, make an appointment, by –

- Phoning our office on 07-34213456; or

- At your convenience, use the linked Book A Meeting facility.

(This article was first published by us in February 2025.)