The Market and Economic Outlook 2015

The market and economic outlook 2015 was prepared to provide our investor clients with a backdrop to the influences that guide our recommendations for the 2015 calendar year. The advisers at ContinuumFP carefully select the managers to invest client monies; and the researchers from whom we take understanding as to the issues that will impact the economy, the markets – and ultimately, the outcome for our clients.

We agree with the general consensus that the market and economic outlook 2015, will be volatile but positive, although likely to be only modestly so. At the same time, there is broad expectation that the global economy will remain sound, with overall growth in the mid-3% range.

Market Outlook

It appears that there is a strong consensus amongst forecasters that 2015 will be a year in which volatility will be a recurring theme: and that feature, used judiciously, should be beneficial to investors. Over the course of the calendar year, most suggest that equities – and to a lesser extent, Listed Property Trusts (LPTs, now known as REITs1) will deliver a positive outcome for the year; but that there will be little movement on interest rates (and by inference, little movement in market valuation of fixed income securities).

Our outlook considers the domestic (Australian) and the global (select other countries of the world) and their contribution to the outlook generally. Central Banks in a number of the select countries affect the markets according to how responsive they are to economic and market conditions: in this regard we are particularly mindful of the US Fed, the ECB (Europe), the BoE (UK), the BoJ (Japan) and the Chinese Central government. The following chart was recently published showing the anticipated levels of the Balance Sheets of the first four of the above named countries.

Our outlook considers the domestic (Australian) and the global (select other countries of the world) and their contribution to the outlook generally. Central Banks in a number of the select countries affect the markets according to how responsive they are to economic and market conditions: in this regard we are particularly mindful of the US Fed, the ECB (Europe), the BoE (UK), the BoJ (Japan) and the Chinese Central government. The following chart was recently published showing the anticipated levels of the Balance Sheets of the first four of the above named countries.

We take the view that terrorism will not play a significant part in economic or market activity by way of shocks (perhaps more wishfully than knowingly), on the basis that market participants are becoming more accustomed to such activity and aware that it rarely changes market standings for any significant period of time. (We acknowledge the social impact of such activity but that is a topic for a different forum.)

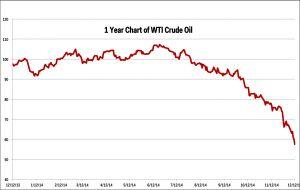

The dramatic reduction in oil prices over the months since October 2014 has had a significant economic impact on economies around the world: different countries are affected according to the extent and type of dependence they have for this resource. Supply countries are seeing inefficient, high-cost producers withdrawing from the industry; consumer countries are witnessing their populations use the reprieve in fuel costs to pay down debt and/ or to increase discretionary spending on other consumer products.

The following graph of the price of West Texas Intermediate Crude oil over the twelve months from December 2013 to December 2014 (from www.businessinsider.com.au) is quite telling: and compares closely with the other oil markets globally.

Expectations are that the oil price (expressed in USDs) will stay in the USD40 to USD60 per barrel for a considerable time, perhaps beyond two years. (Our oil comes through an Asian market, is usually somewhat higher priced than quoted for the US – and whilst quoted in USDs generally, its cost to the Australian consumer is impacted by the currency exchange movement of the AUD to the USD.)

To participate in the broad picture outcome as we perceive likely market and economic outlook 2015, a diversified portfolio embracing global as well as domestic investment assets is going to be required. The elements of a diversified portfolio will include –

Equities (Shares)

Domestically, we believe that the Australian Stock Exchange will show some volatility, will continue to generate around 4.5% in dividend yield (which can be grossed up to around 6.0% including the franking credits) and probably experience growth in valuation in keeping with inflation (around 2.5% to 3.0%). This would see us with an ASX All Ords at around the 6,100 mark in late December 2015.

Globally the picture is somewhat clouded when we consider markets other than those on Wall Street: our best guess prediction though is that Europe as a whole (including the UK) will probably be flat over the year as the various economies struggle with minimal economic growth; Japan could put up some growth, subject to the next phase of ‘Abenomics’ being successful; Asia broadly is expected to struggle in the face of the highly valued USD and slower economic growth; other Emerging Markets will struggle with the same ‘headwinds’; and Frontier Markets may generate a positive outcome if only on the basis of coming off a low base. Overall, we expect growth on these equity markets, including a positive outcome for the US, to be in the mid-single digits range of 4% to 7%.

Listed Property Trusts (now known as REITs)

Domestically, whilst interest rates are at historic lows in Australia, we believe REITs will add some value during 2015, albeit at low to middle single digits (around 3% to 6%): on an income basis, a yield of up to 4% on recent values is anticipated. Until the downturn occasioned by the reduction in office space demand from the mining sector is offset by increased demand from other industrial or commercial sectors, this position could prevail beyond 2015.

Globally, we perceive some correlation with the global equity markets, with the exception that the UK may in fact provide more capital growth in their REITs than will the rest of Europe. The US REITs are expected to perform similarly to the Australian REITs, with perhaps better growth factor but modest yield on recent values. We expect this performance to persist into 2016 as economic activity remains sub-par.

Fixed Income Securities

Domestically, yields are expected to stay low for the balance of 2015 as the RBA persists with the historically low rate for its dealing with its customers – and whilst they held in early March, further cuts are expected during 2015, in spite of the status of residential housing market valuations. This will encourage corporate borrowings with companies seeking to lock in low funding costs for extended periods into the future.

Globally, apart from veiled ‘threats’ by the US Federal Reserve to increase the cash rate at some time during this year, Central Banks in other major economies are still either reducing their official rates or printing more money – and accordingly we don’t anticipate any improvement in yields from these securities for some time to come: and certainly not during 2015. Long-term holders of higher yielding coupon bonds will be benefiting from higher valuation of their investment during this phase.

Cash

The outlook for cash is fairly much aligned with that for Fixed Income securities both domestically and globally: we anticipate little change in the interest crediting rates on most bank deposits, and perhaps some slight further downward pressure on term deposits during the course of 2015. (This latter position could change later in the calendar year as a position in relation the central banks starting any ‘tightening’ late in the year or anticipated in the early part of 2016 becomes clearer.)

Alternatives (including Commodities, Infrastructure and hybrids)

Whilst this is a very broad asset class we believe that it is going to be a positive contributor to portfolio growth for the 2015 calendar year, particularly if governments around the world decide to add stimulus to their economies that will lead to an increase in demand for commodities; and to the extent that they undertake productive infrastructure projects, increase the demand for labour – and for machinery and materials – to construct them should give us this outcome. We hold this view both domestically and globally.

Depending on the aversion an investor has to market and asset risks, a diversified portfolio constructed by a financial adviser will comprise the above asset classes allocated around the following proportions:

Continuum Financial Planners’ representation of typical Asset Allocations according to Investor Risk Aversion

Economic Outlook

Broad Overview

In considering the market and economic outlook 2015, the market is recognised as an advance warning of probable economic conditions for the year (some say, between three and seven months advance when reading the equity market): hence we provide our understanding of the forecasts economists are giving for the year.

There are many factors that influence the economic drivers within countries and between them in their trading relationships. Amongst them are availability of affordable funding, business and consumer confidence, supply and demand considerations, stability of government and acceptable ‘rule of law’.

For 2015 we are confronted with governments around the world who, like ours are unable to govern with a clear control of the country’s destiny because of the impact of ‘hung parliaments’ and/ or opposition-party controlled houses of review (in our case, the Senate): this situation leads to unstable government and restrains business confidence because of the uncertainty as to what economic policies are likely to prevail for the foreseeable future.

Also impacting the global situation are events such as military conflict (consider the Middle East, Ukraine and parts of Africa); commodities price collapse (consider iron ore, oil and some cereal crops); and currency ‘wars’ (consider deliberate action by Japan to lower the value of the Yen; concern that China manipulates the value of the Renminbi; and the inability of less-economically viable members of the European block to reduce their currency as they are constrained by the Euro).

Assessing all of the relevant factors, we are of the view that global economic growth will be subdued when compared with long-term averages and accept the IMF view that it could be as low as 3.4%2 for 2015. (See Infographic for summary dashboard of IMF’s revised World Economic Outlook published in January 2015.)

Domestic Outlook

We expect that the Australian economy will have another slow year for 2015 and that efforts to improve efficiency and productivity will be hampered by the lack of demand by consumers: and the lack of commitment by corporates and/ or governments to undertake major works.

Much has been written about the cessation of the mining resources exploration and extraction infrastructure construction projects – and about the reduced sale price attainable for the output from the mines (established during that boom up until late in 2014) – and the fact that the Australian economy is transitioning to another phase, more services based: this transition is taking longer than anticipated and we expect 2015 to remain fairly flat, with a possible year-on-year GDP outcome around 2% to 2.5% for calendar 2015.

Global Outlook

Australia’s contribution to the global economy is in the order of 5% (note: we represent less than 2% of global investment markets!) and so if our contribution to global economic activity for 2015 is .04% of the 3% we mention in the overview above, you might ask where the other 2.96% is going to come from? The four ‘powerhouses’ of global economic activity are arguably, the USA (23%), Europe (19%), China(9.3%) and Japan (8.7%)3, together contributing 60% of the world’s economic activity between them: with the USA expecting growth at sub-4% for 2015 and the others respectively sub-2%, 7% and sub-3% their contribution to the global forecast is shaping up to be around 1.73% we are still looking to ‘the rest of the world’ to contribute another 1.23%.

We will be looking to India, South Korea, Asia (ex-japan, China and South Korea), Russia and OPEC member countries4 to provide the bulk of this.

Concluding observation

In many of the articles that have been published on our website articles Library, we have referred to the equities market phenomenon of foretelling the direction of the economy: we believe that depending on the cyclical status of the economy at the relevant time, the equities market gives an indication about five to nine months in advance of an economic event. Whilst there may appear to be a disconnect between the anticipated GDP growth (economic activity globally) and the predictive characteristic of the equities market, bear in mind that economies include non-productive as well as productive sectors and internal transfers for welfare and administration purposes are funded from the economic activity of the corporations represented in the stock markets.

1 Real Estate Investment Trusts (REITs)

2 International Monetary Fund World Economic Outlook Update: released 20 January 2015.

3 Extracted from January 2012 publication by the University of Illinois Department of Agricultural and Consumer Economics ‘Country Contribution to World Economic Activity and Growth’: http://farmdocdaily.illinois.edu/2012/01/country-contribution-to-world.html

4 The twelve members of OPEC are not recognised as significant economies other than for their oilfield spoils.