Boosting Retirement Savings with Tax-Effective Strategies

For many Australians, superannuation is one of the most effective ways to build long-term wealth for retirement. While employer Super Guarantee (SG) contributions form the foundation of most retirement savings plans, other superannuation concessional contributions will improve the lifestyle you will enjoy in retirement.

Making additional concessional contributions to super can help grow your retirement savings in a tax-effective way while potentially reducing your personal income tax.

What Are Concessional Contributions?

Concessional contributions are contributions made to your super from before-tax income. They generally include:

- employer Super Guarantee contributions,

- salary sacrifice contributions,

- additional employer contributions, and

- personal contributions claimed as a tax deduction.

These contributions are usually taxed at 15% within the super fund, which is often lower than an individual’s marginal tax rate.

This concessional tax treatment is one of the key advantages of investing through the superannuation system.

Key Benefits of Concessional Contributions

Tax Advantages

For many investors, concessional contributions can reduce taxable income while increasing retirement savings.

If your marginal tax rate is above 15%, directing some income into super through salary sacrifice or deductible personal contributions may reduce the amount of tax you pay overall.

For example, rather than paying your marginal tax rate on employment income, concessional contributions are generally taxed at 15% when received by the super fund.

Higher income earners should note that an additional 15% tax may apply to some or all concessional contributions if income and concessional contributions exceed relevant legislative thresholds.

Accelerating Retirement Savings

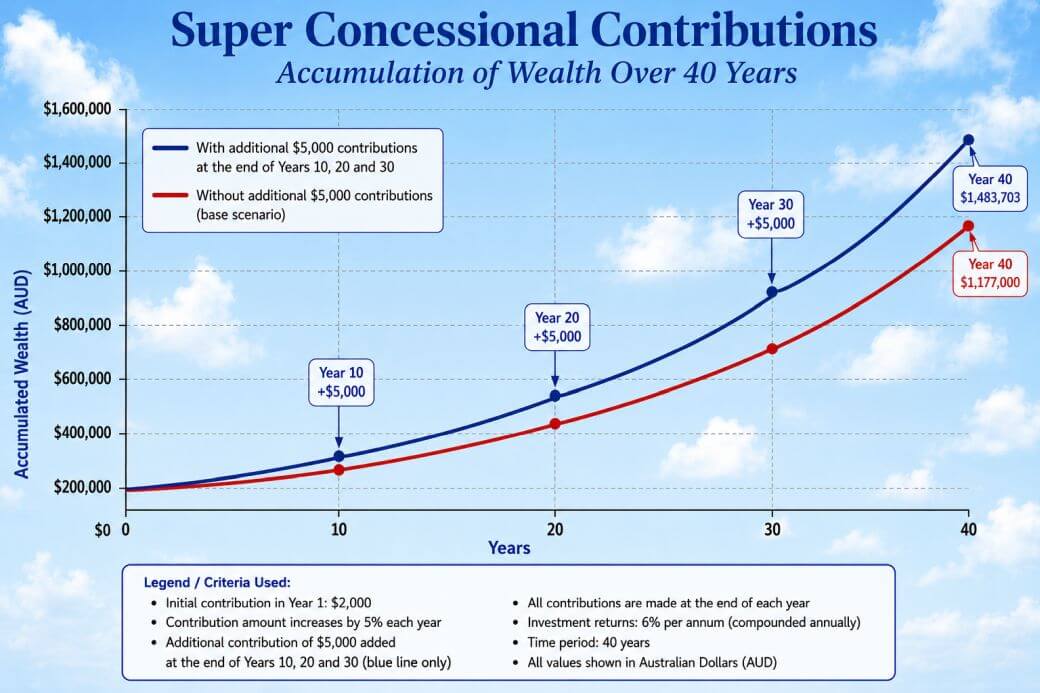

Additional contributions can significantly improve long-term retirement outcomes due to the power of compounding returns over time.

Even modest regular contributions may help build a larger retirement balance, particularly when started earlier in life.

(These considerations are clearly exemplified in the graph above.)

Flexibility Through Carry Forward Rules

If your total super balance was below the relevant legislative threshold on 30 June of the previous financial year, you may be able to carry forward unused concessional contribution cap amounts from up to five (5) previous financial years.

This strategy can be valuable for people with fluctuating income or changing work patterns, including:

- business owners and sole traders,

- parents returning to work,

- individuals receiving bonuses or inheritances, and

- investors realising large capital gains.

The carry forward rule may allow you to make larger tax-deductible super contributions in higher-income years while remaining within contribution limits.

Contribution Caps Matter

Concessional contribution caps apply across all of your superannuation accounts combined and include:

- employer Super Guarantee contributions,

- salary sacrifice contributions, and

- deductible personal contributions.

Contribution caps and thresholds can change over time, so investors should refer to the Australian Taxation Office superannuation contribution caps page for current limits and eligibility rules.

Exceeding the concessional contribution cap can result in additional tax and administrative complexity.

If you exceed the concessional contributions cap:

- the excess amount is generally added to your taxable income,

- you may receive a tax offset for contributions tax already paid,

- you may be able to withdraw part of the excess contributions from super, or

- leave the excess in super, where it may count toward your non-concessional contribution cap.

Careful planning and contribution monitoring are essential to avoid unintended tax consequences.

Timing Is Critical

A common mistake involves misunderstanding when a contribution is counted.

Concessional contributions count toward the financial year in which the super fund receives and accepts the contribution — not when the payment is initiated.

This is particularly important near 30 June, as electronic transfers and BPAY payments can take several business days to process.

To claim a tax deduction for a personal contribution in a financial year, the contribution must be received by the super fund before 30 June.

Contributing earlier to allow additional processing time can help avoid accidental cap breaches or missed deductions.

Comparing Salary Sacrifice vs Personal Deductible Contributions

Salary Sacrifice

This strategy involves directing part of your future before-tax salary into super through your employer.

Potential advantages include:

- reducing taxable income,

- building super gradually throughout the year, and

- automatic and disciplined investing.

Personal Deductible Contributions

Personal deductible contributions may suit individuals who:

- are self-employed,

- receive irregular income,

- prefer flexibility over contribution timing, or

- cannot access salary sacrifice arrangements.

To claim a deduction, you must generally submit a valid Notice of Intent to Claim form to your super fund before lodging your tax return.

Important Considerations Before Contributing More to Super

While superannuation offers attractive tax benefits, it is a long-term investment structure with preservation rules.

Generally, money contributed to super cannot be accessed until a condition of release is met, such as retirement after reaching preservation age.

Before making large concessional contributions, investors should consider:

- cash flow needs,

- mortgage and debt priorities,

- emergency savings,

- upcoming large expenses,

- overall investment strategy, and

- contribution cap limits.

Superannuation should form part of a broader financial plan rather than being considered in isolation.

Why Professional Advice Matters

Concessional contribution strategies can deliver significant long-term benefits, but they require careful planning and monitoring.

Professional financial advice can help you:

- structure contributions tax-effectively,

- avoid exceeding contribution caps,

- use carry forward rules strategically,

- coordinate super with broader investment goals,

- understand preservation and access rules, and

- align retirement strategies with your personal objectives.

Tax rules, contribution caps, eligibility requirements and superannuation legislation can change over time. Seeking professional advice helps ensure your strategy remains appropriate for your circumstances and objectives.

By using concessional contributions strategically, investors may improve retirement outcomes while benefiting from the tax advantages available within Australia’s superannuation system.

The ContinuumFP Way

Superannuation and retirement planning strategies are key areas of advice provided by the experienced advisers at Continuum Financial Planners.

Whether you are looking to boost retirement savings, improve tax efficiency or better structure your long-term financial strategy, our team can help develop a personalised approach aligned with your goals and circumstances.

To arrange an appointment:

- Phone our office on 07 3421 3456, or

- Use our online Book a Meeting facility.

(This article was first posted by us in May 2026.)